During the Q2 earnings call, when asked whether Moderna was considering M&A deals in China or other regions, CEO Stéphane Bancel flatly denied the possibility. Such a blunt dismissal of potential strategic options is rare among corporate executives.

Bancel argued that partnerships, rather than M&A, are Moderna’s preferred approach to acquiring non-mRNA technology assets. For instance, Moderna has already collaborated with Merck (MSD) in oncology to advance mRNA-4157, Moderna’s personalized mRNA cancer vaccine, in combination with Keytruda (an anti-PD-1 monoclonal antibody) into Phase 3 trials—making it the world’s first mRNA cancer vaccine to reach this stage. Results from this trial are expected next year, with potential market approval by 2027. Until then, Moderna’s primary revenue will continue to rely on sales of other vaccine products. Bancel also revealed that the company plans to launch eight new products within the next three years.

However, capital markets remain skeptical of Moderna’s business strategy. Its market capitalization has plummeted from a peak of nearly $200 billion to just under $10.7 billion today—a drop of over 90%. This reflects waning investor confidence in the post-pandemic rebound of COVID-19 and respiratory syncytial virus (RSV) vaccine sales.

Source: Xueqiu.com

Source: Xueqiu.com

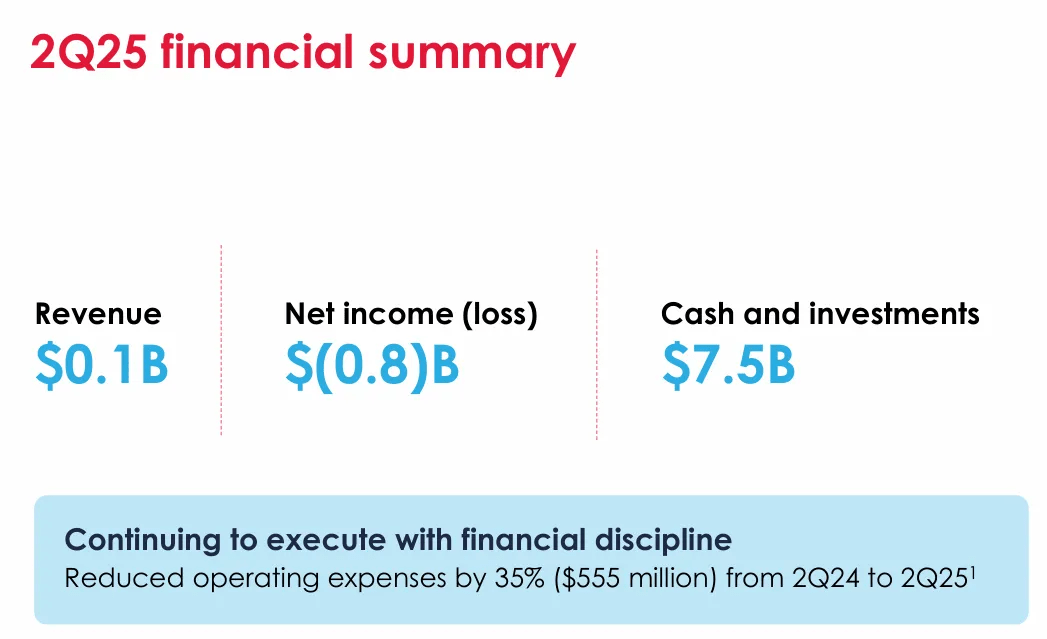

The concerns are not unfounded. With COVID-19 vaccine sales in freefall, Moderna’s Q2 revenue dropped to $142 million, down 41% year-over-year, while net losses reached $825 million. Faced with such financial challenges, Bancel’s reluctance to pursue M&A deals is understandable. To address the crisis, Moderna announced a 10% workforce reduction, bringing total headcount below 5,000. This move was not entirely unexpected—as early as May, the company had signaled plans to cut annual operating expenses by approximately $1.5 billion by 2027.

Source: Moderna Official Website

Source: Moderna Official Website

In contrast, BioNTech, the German mRNA vaccine maker that also rose rapidly during the pandemic, has adjusted its strategy post-crisis and won back investor confidence. Over the past year, BioNTech’s stock has surged nearly 25%, and as of August 1, 2025, its market cap has surpassed $26.6 billion—roughly double that of Moderna.

Despite both companies possessing world-leading mRNA technology platforms, their development paths have diverged sharply. Unlike Moderna’s continued focus on expanding its mRNA vaccine pipeline, BioNTech, after its COVID-19 vaccine success, shifted decisively toward the more promising field of oncology—such as its mRNA melanoma vaccine BNT111.

Moreover, BioNTech has adopted a more diversified R&D and commercial strategy: enriching its pipeline through licensing deals while aggressively entering hot new anticancer drug areas like ADCs, creating synergies with its existing mRNA cancer vaccine platform.

Moderna, on the other hand, failed to leverage its pandemic windfall to diversify its product pipeline. Now, as the world enters the post-pandemic era, companies that once thrived on COVID-related products face the daunting challenge of reinvention and sustainable growth. How will Moderna climb back to its $100 billion valuation peak? The pharmaceutical industry will be watching closely.

发布者:sima,转载请首先联系contact@drugtimes.cn获得授权

为好文打赏 支持药时代 共创新未来!

为好文打赏 支持药时代 共创新未来!